Factor Analysis with Alphalens#

Factor investing is the idea that you can rank stocks by some measurable characteristic – a “factor” – and that stocks with high factor values tend to outperform those with low factor values (or vice versa). Classic factors include:

Momentum: stocks that have gone up tend to keep going up

Value: cheap stocks (relative to fundamentals) tend to outperform

Size: small-cap stocks have historically earned higher returns

Quality: profitable, low-leverage firms tend to outperform

But how do you test whether a factor actually works? That’s where alphalens comes in. Originally built by Quantopian and now maintained as alphalens-reloaded, it provides a structured framework for evaluating alpha factors.

The key question alphalens answers: does my factor predict future returns?

Setup#

We’ll use alphalens-reloaded along with our usual tools. If you need to install it:

pip install alphalens-reloaded

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import alphalens

from alphalens.utils import get_clean_factor_and_forward_returns

from alphalens.tears import create_returns_tear_sheet, create_information_tear_sheet, create_turnover_tear_sheet

import warnings

warnings.filterwarnings('ignore')

%matplotlib inline

The Data#

We need daily prices for a universe of stocks. We’ll use 100 large-cap U.S. stocks – mostly S&P 500 components – over a six-year period. This gives us enough history to compute trailing 12-month momentum and still have several years of forward returns to analyze.

# 100 large-cap U.S. stocks

tickers = [

'AAPL', 'MSFT', 'AMZN', 'NVDA', 'GOOGL', 'META', 'BRK-B', 'UNH', 'JNJ', 'V',

'XOM', 'JPM', 'PG', 'MA', 'HD', 'CVX', 'MRK', 'ABBV', 'LLY', 'PEP',

'KO', 'COST', 'AVGO', 'WMT', 'MCD', 'CSCO', 'CRM', 'ACN', 'ABT', 'TMO',

'LIN', 'DHR', 'CMCSA', 'NKE', 'VZ', 'ADBE', 'TXN', 'NEE', 'PM', 'RTX',

'BMY', 'UPS', 'HON', 'LOW', 'QCOM', 'UNP', 'SPGI', 'INTC', 'AMGN', 'BA',

'CAT', 'GS', 'ELV', 'BLK', 'DE', 'ISRG', 'MDLZ', 'GILD', 'SYK', 'ADI',

'ADP', 'MMC', 'TJX', 'SCHW', 'VRTX', 'PLD', 'REGN', 'CI', 'CB', 'ZTS',

'SO', 'DUK', 'BDX', 'CME', 'CL', 'MO', 'ITW', 'SLB', 'EOG', 'PNC',

'AON', 'PYPL', 'WM', 'APD', 'ICE', 'SHW', 'FDX', 'MCK', 'NSC', 'EMR',

'GD', 'PSX', 'CCI', 'KMB', 'AEP', 'D', 'F', 'GM', 'TROW', 'USB'

]

print(f"Universe: {len(tickers)} stocks")

Universe: 100 stocks

# Load cached prices (or download from yfinance)

import os

DATA_FILE = os.path.join('..', 'data', 'alphalens_prices.csv')

if os.path.exists(DATA_FILE):

prices = pd.read_csv(DATA_FILE, index_col=0, parse_dates=True)

print(f"Loaded cached data: {prices.shape[0]} days, {prices.shape[1]} stocks")

else:

import yfinance as yf

data = yf.download(tickers, start='2018-01-01', end='2024-01-01', auto_adjust=True)

prices = data['Close'].copy()

threshold = int(len(prices) * 0.9)

prices = prices.dropna(axis=1, thresh=threshold)

prices = prices.dropna()

print(f"Downloaded: {prices.shape[0]} days, {prices.shape[1]} stocks")

prices.head()

Loaded cached data: 1509 days, 100 stocks

| AAPL | ABBV | ABT | ACN | ADBE | ADI | ADP | AEP | AMGN | AMZN | ... | UNP | UPS | USB | V | VRTX | VZ | WM | WMT | XOM | ZTS | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2018-01-02 | 40.304180 | 69.343704 | 50.822933 | 136.707809 | 177.699997 | 77.602295 | 97.942848 | 54.101383 | 137.775131 | 59.450500 | ... | 113.271820 | 89.841110 | 39.419216 | 108.111893 | 152.910004 | 34.220016 | 75.054367 | 28.914417 | 58.580414 | 67.104774 |

| 2018-01-03 | 40.297146 | 70.428848 | 50.935322 | 137.338791 | 181.039993 | 78.565025 | 99.006836 | 53.645611 | 140.374969 | 60.209999 | ... | 113.905869 | 91.831604 | 39.805889 | 109.188210 | 152.009995 | 33.516830 | 76.144005 | 29.166634 | 59.730938 | 67.413315 |

| 2018-01-04 | 40.484337 | 70.027206 | 50.848877 | 138.964981 | 183.220001 | 78.479057 | 99.952545 | 53.010529 | 139.783432 | 60.479500 | ... | 113.288536 | 92.427330 | 40.112324 | 109.594208 | 153.070007 | 33.625507 | 76.797791 | 29.193029 | 59.813625 | 67.815369 |

| 2018-01-05 | 40.945263 | 71.246231 | 50.995834 | 140.111313 | 185.339996 | 78.797089 | 99.893456 | 52.898464 | 140.616302 | 61.457001 | ... | 114.731720 | 92.710632 | 40.360378 | 112.218849 | 155.690002 | 33.548794 | 76.701866 | 29.366070 | 59.765388 | 68.591415 |

| 2018-01-08 | 40.793182 | 70.104713 | 50.848877 | 141.231003 | 185.039993 | 78.934647 | 99.589455 | 53.361683 | 140.577377 | 62.343498 | ... | 116.325127 | 93.836624 | 40.418739 | 112.672050 | 156.889999 | 33.491261 | 76.754196 | 29.800125 | 60.034073 | 69.414192 |

5 rows × 100 columns

Building a Momentum Factor#

We’ll construct the classic 12-1 momentum factor from Jegadeesh and Titman (1993). The idea:

Look at each stock’s return over the past 12 months

Skip the most recent month (this avoids short-term reversal effects)

Rank stocks by this trailing return

Go long the top quartile (25 stocks) and short the bottom quartile (25 stocks)

Why skip the most recent month? There’s a well-documented short-term reversal effect – stocks that went up last month tend to fall back a bit, and vice versa. The 12-1 momentum factor isolates the medium-term trend.

# Step 1: Get month-end prices

monthly_prices = prices.resample('ME').last()

print(f"Monthly prices: {monthly_prices.shape[0]} months, {monthly_prices.shape[1]} stocks")

# Step 2: Compute 12-1 momentum

# shift(1) skips the most recent month

# pct_change(11) gives the return over the prior 11 months

# Together: return from t-12 to t-1

momentum = monthly_prices.shift(1).pct_change(11)

momentum = momentum.dropna(how='all')

print(f"Momentum signals: {momentum.shape[0]} months")

momentum.tail()

Monthly prices: 72 months, 100 stocks

Momentum signals: 60 months

| AAPL | ABBV | ABT | ACN | ADBE | ADI | ADP | AEP | AMGN | AMZN | ... | UNP | UPS | USB | V | VRTX | VZ | WM | WMT | XOM | ZTS | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2023-08-31 | 0.255240 | 0.157580 | 0.105357 | 0.114442 | 0.462537 | 0.335151 | 0.032701 | -0.130609 | -0.000891 | 0.054508 | ... | 0.053927 | -0.010977 | -0.084409 | 0.203731 | 0.250497 | -0.128863 | -0.014737 | 0.220161 | 0.149497 | 0.212258 |

| 2023-09-30 | 0.367471 | 0.139423 | 0.083849 | 0.278710 | 1.032485 | 0.322790 | 0.144114 | -0.058048 | 0.175546 | 0.221327 | ... | 0.161363 | 0.087818 | -0.057553 | 0.394074 | 0.203081 | -0.015431 | -0.008708 | 0.272933 | 0.315561 | 0.296083 |

| 2023-10-31 | 0.123162 | 0.048804 | -0.007039 | 0.094402 | 0.600942 | 0.250723 | 0.016758 | -0.111366 | 0.027580 | 0.240922 | ... | 0.059551 | -0.036235 | -0.177736 | 0.119237 | 0.114551 | -0.088483 | -0.020554 | 0.140859 | 0.096134 | 0.161611 |

| 2023-11-30 | 0.158539 | -0.088700 | -0.103537 | 0.002925 | 0.542516 | -0.067625 | -0.156092 | -0.196989 | -0.083455 | 0.378599 | ... | -0.020547 | -0.234876 | -0.258444 | 0.089694 | 0.144469 | -0.032574 | -0.003020 | 0.088516 | -0.025759 | 0.027846 |

| 2023-12-31 | 0.470113 | -0.083335 | -0.031093 | 0.268299 | 0.815618 | 0.133913 | -0.021482 | -0.128067 | 0.062236 | 0.739167 | ... | 0.109108 | -0.093195 | -0.087323 | 0.245275 | 0.228652 | 0.044297 | 0.109343 | 0.110655 | -0.036738 | 0.216524 |

5 rows × 100 columns

Each value in the table above is the trailing 12-1 month return for that stock. For example, a value of 0.30 means the stock went up 30% over the past year (excluding the most recent month). A value of -0.15 means it fell 15%.

The momentum strategy says: buy the winners and sell the losers.

Preparing Data for Alphalens#

Alphalens expects the factor data in a specific format: a pandas Series with a MultiIndex of (date, asset). Each entry is the factor value for that stock on that date.

We also need to make sure our factor dates are actual trading days (days that appear in our daily price data), since alphalens uses the daily prices to compute forward returns.

# Get the last trading day of each month from our price data

month_end_trading = prices.resample('ME').last().index

# Forward-fill momentum to daily dates, then keep only month-end trading days

momentum_daily = momentum.reindex(prices.index, method='ffill')

momentum_filtered = momentum_daily.loc[momentum_daily.index.isin(month_end_trading)]

# Stack into the MultiIndex format alphalens expects

factor = momentum_filtered.stack()

factor.index.names = ['date', 'asset']

factor = factor.dropna()

factor.name = 'momentum'

print(f"Factor observations: {len(factor):,}")

print(f"Unique dates: {factor.index.get_level_values('date').nunique()}")

print(f"Unique assets: {factor.index.get_level_values('asset').nunique()}")

Factor observations: 4,200

Unique dates: 42

Unique assets: 100

# Look at the factor for one date

sample_date = factor.index.get_level_values('date').unique()[12]

sample = factor.loc[sample_date].sort_values()

print(f"Factor values on {sample_date.strftime('%Y-%m-%d')}:")

print(f" Bottom 5 (short candidates): ")

print(sample.head().to_string())

print(f"\n Top 5 (long candidates):")

print(sample.tail().to_string())

Factor values on 2020-07-31:

Bottom 5 (short candidates):

asset

SLB -0.515902

BA -0.453004

EOG -0.400135

XOM -0.362814

GM -0.351930

Top 5 (long candidates):

asset

PYPL 0.578170

AAPL 0.732790

VRTX 0.742348

REGN 1.046364

NVDA 1.257990

Running Alphalens#

The core function is get_clean_factor_and_forward_returns(). It takes our factor and pricing data and:

Computes forward returns at specified horizons (we’ll use 5, 10, and 21 trading days – roughly 1 week, 2 weeks, and 1 month)

Sorts stocks into quantiles based on the factor value (we’ll use 4 quantiles, so Q1 is the bottom 25% and Q4 is the top 25%)

Aligns everything into a clean DataFrame

factor_data = get_clean_factor_and_forward_returns(

factor,

prices,

quantiles=4,

periods=(5, 10, 21)

)

factor_data.head(10)

Dropped 2.4% entries from factor data: 2.4% in forward returns computation and 0.0% in binning phase (set max_loss=0 to see potentially suppressed Exceptions).

max_loss is 35.0%, not exceeded: OK!

| 5D | 10D | 21D | factor | factor_quantile | ||

|---|---|---|---|---|---|---|

| date | asset | |||||

| 2019-01-31 | AAPL | 0.027037 | 0.030597 | 0.061068 | -0.043731 | 3 |

| ABBV | -0.013949 | 0.002865 | -0.010337 | -0.152533 | 2 | |

| ABT | -0.003289 | 0.013565 | 0.077281 | 0.179296 | 4 | |

| ACN | 0.010615 | 0.028004 | 0.060371 | -0.106692 | 2 | |

| ADBE | 0.023888 | 0.049714 | 0.041724 | 0.132559 | 4 | |

| ADI | 0.017904 | 0.056949 | 0.104762 | -0.046901 | 3 | |

| ADP | 0.041762 | 0.059425 | 0.095967 | 0.083032 | 4 | |

| AEP | 0.012737 | 0.011462 | 0.037848 | 0.127235 | 4 | |

| AMGN | -0.015392 | 0.005416 | 0.022112 | 0.077078 | 4 | |

| AMZN | -0.060719 | -0.055902 | -0.013126 | 0.035206 | 3 |

Each row is a (date, asset) observation. The columns are:

5D, 10D, 21D: Forward returns at each horizon (what the stock actually returned after the signal)

factor: The momentum score

factor_quantile: Which quartile (1 = lowest momentum, 4 = highest momentum)

If momentum works, we’d expect Q4 stocks (winners) to have higher forward returns than Q1 stocks (losers).

Returns Analysis#

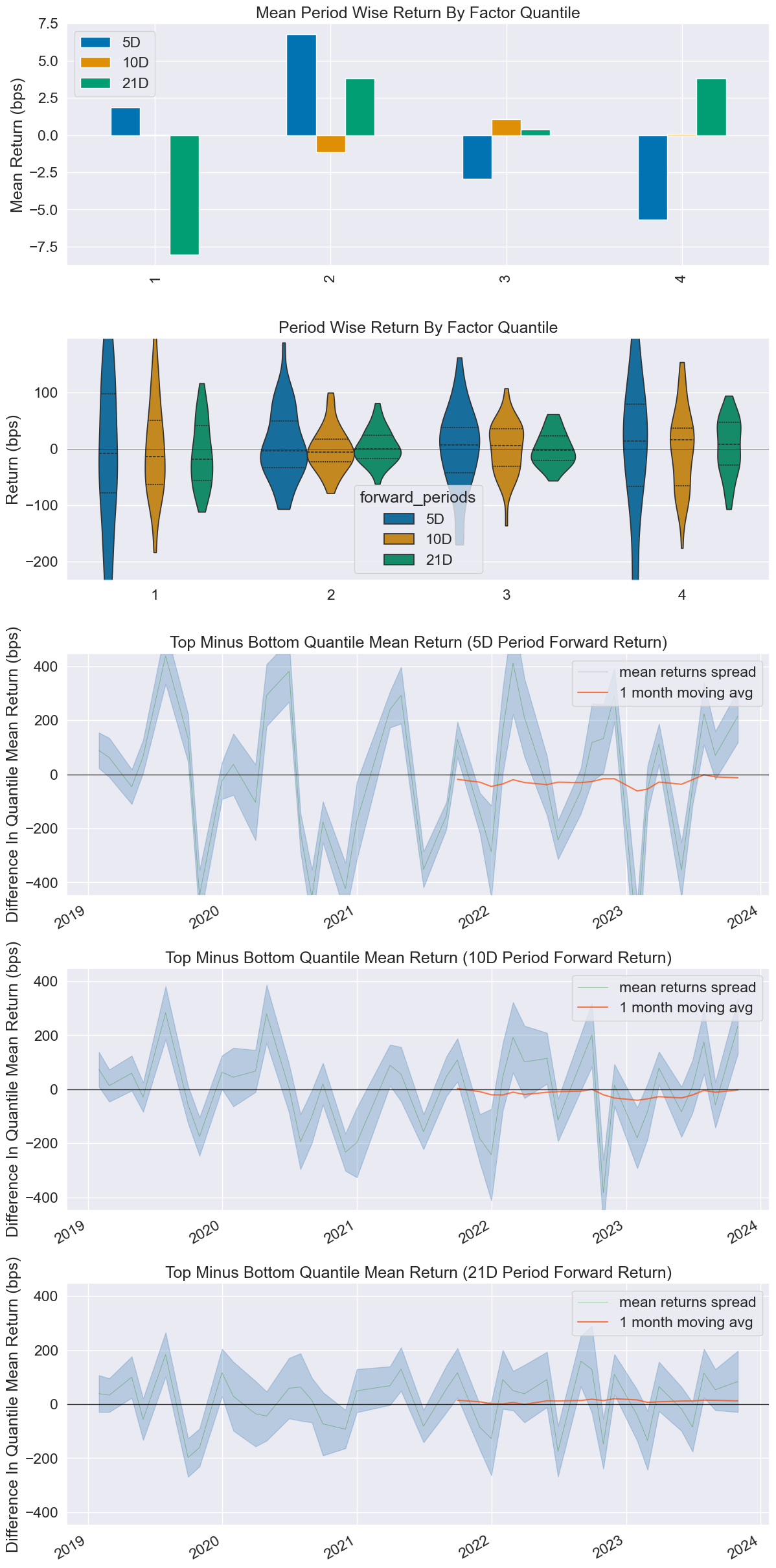

The returns tear sheet shows us the average return by quantile. This is the most important output – it tells us whether the factor actually predicts returns.

create_returns_tear_sheet(factor_data)

Returns Analysis

| 5D | 10D | 21D | |

|---|---|---|---|

| Ann. alpha | -0.007 | 0.031 | 0.050 |

| beta | -0.109 | -0.104 | -0.114 |

| Mean Period Wise Return Top Quantile (bps) | -5.661 | 0.060 | 3.809 |

| Mean Period Wise Return Bottom Quantile (bps) | 1.837 | 0.012 | -8.039 |

| Mean Period Wise Spread (bps) | -7.498 | 0.150 | 11.995 |

<Figure size 640x480 with 0 Axes>

Reading the Output#

Look at the Mean Period Wise Return by Factor Quantile chart. A good momentum factor shows a clear staircase pattern: Q1 (bottom) has the lowest returns and Q4 (top) has the highest.

The Returns Analysis table at the top shows:

Mean Period Wise Return Top Quantile (bps): Average return of the top quartile in basis points

Mean Period Wise Return Bottom Quantile (bps): Average return of the bottom quartile

Mean Period Wise Spread (bps): The difference (long top, short bottom) – this is your strategy’s return

A positive spread at the 21D horizon means that momentum had some predictive power over a monthly horizon in this sample.

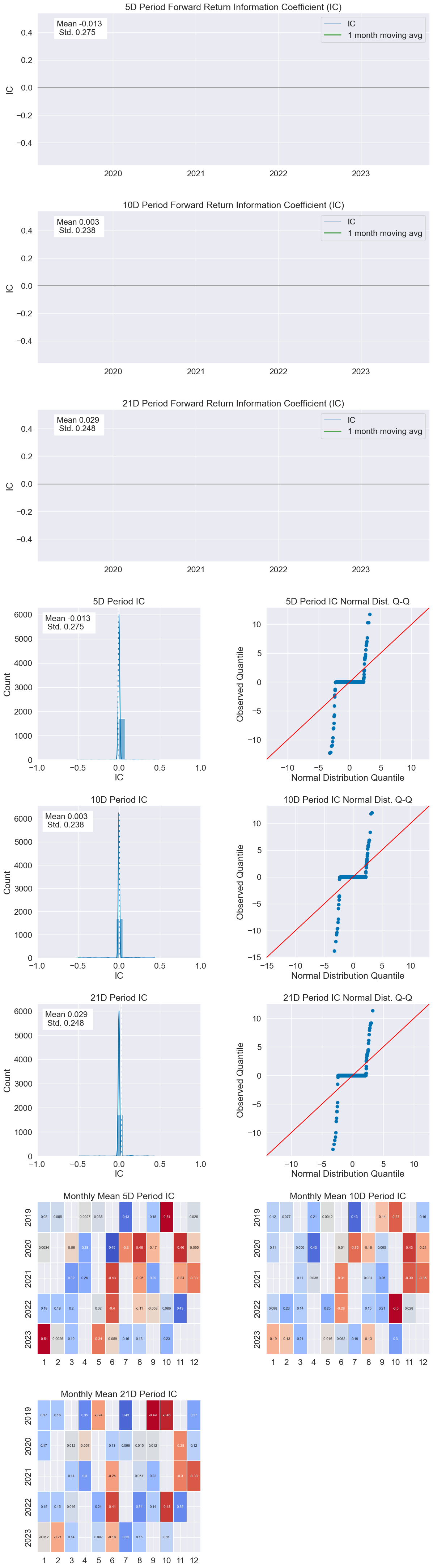

Information Coefficient (IC)#

The Information Coefficient measures the rank correlation (Spearman) between the factor value and forward returns. An IC of 0.05 might sound small, but in practice, even IC values between 0.02 and 0.05 can be economically meaningful – you’re trying to find a small, persistent edge across many stocks.

create_information_tear_sheet(factor_data)

Information Analysis

| 5D | 10D | 21D | |

|---|---|---|---|

| IC Mean | -0.013 | 0.003 | 0.029 |

| IC Std. | 0.275 | 0.238 | 0.248 |

| Risk-Adjusted IC | -0.047 | 0.012 | 0.118 |

| t-stat(IC) | NaN | NaN | NaN |

| p-value(IC) | NaN | NaN | NaN |

| IC Skew | NaN | NaN | NaN |

| IC Kurtosis | NaN | NaN | NaN |

<Figure size 640x480 with 0 Axes>

The IC heatmap shows whether the factor’s predictive power is consistent over time or concentrated in certain periods. The IC histogram shows the distribution of monthly IC values – ideally, most values should be positive (for a long-momentum factor).

Note that we only have a limited sample here. Professional quant researchers would use much longer histories and more sophisticated factor construction.

Turnover Analysis#

Turnover measures how much the portfolio changes each period. High turnover means you’re trading a lot, which means high transaction costs. A factor can look great before costs but be unprofitable after accounting for trading.

create_turnover_tear_sheet(factor_data)

Turnover Analysis

| 5D | 10D | 21D | |

|---|---|---|---|

| Quantile 1 Mean Turnover | NaN | NaN | NaN |

| Quantile 2 Mean Turnover | NaN | NaN | NaN |

| Quantile 3 Mean Turnover | NaN | NaN | NaN |

| Quantile 4 Mean Turnover | NaN | NaN | NaN |

| 5D | 10D | 21D | |

|---|---|---|---|

| Mean Factor Rank Autocorrelation | NaN | NaN | NaN |

<Figure size 640x480 with 0 Axes>

<Figure size 1400x12600 with 0 Axes>

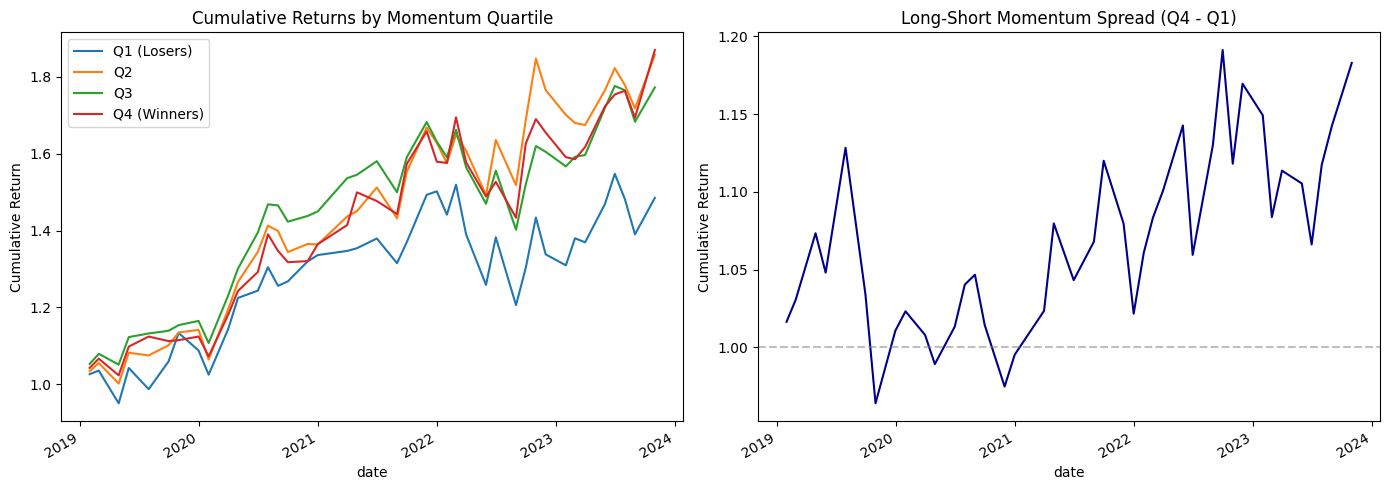

Building the Long-Short Portfolio#

Now let’s see what a practical long-short momentum strategy looks like. Each month, we:

Rank all 100 stocks by 12-1 momentum

Go long the top 25 (Q4)

Go short the bottom 25 (Q1)

Equal-weight within each leg

# Compute monthly returns for each quantile

quantile_returns = factor_data.groupby(

[factor_data.index.get_level_values('date'), 'factor_quantile']

)['21D'].mean().unstack('factor_quantile')

# Long-short spread: Q4 - Q1

quantile_returns['Long-Short'] = quantile_returns[4] - quantile_returns[1]

# Cumulative returns

cumulative = (1 + quantile_returns).cumprod()

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Plot cumulative returns by quantile

cumulative[[1, 2, 3, 4]].plot(ax=axes[0])

axes[0].set_title('Cumulative Returns by Momentum Quartile')

axes[0].set_ylabel('Cumulative Return')

axes[0].legend(['Q1 (Losers)', 'Q2', 'Q3', 'Q4 (Winners)'])

# Plot long-short spread

cumulative['Long-Short'].plot(ax=axes[1], color='darkblue')

axes[1].set_title('Long-Short Momentum Spread (Q4 - Q1)')

axes[1].set_ylabel('Cumulative Return')

axes[1].axhline(y=1, color='gray', linestyle='--', alpha=0.5)

plt.tight_layout();

Does Momentum Work?#

The results above are mixed – and that’s the point. A few things to consider:

Sample period matters: Momentum tends to work well during trending markets but suffers sharp reversals during market crashes and recoveries (“momentum crashes”). Our sample includes COVID-19, which created a massive momentum reversal.

Transaction costs: We haven’t accounted for the cost of trading 50 stocks each month. Momentum strategies have relatively high turnover, which eats into returns.

Survivorship bias: Our universe only includes stocks that are large today. Some of the best momentum stocks from 2018 might have been smaller then, and some 2018 large-caps may have declined and left the index. This biases our results.

Data snooping: We picked momentum because we know it’s a famous factor. If we’d tested hundreds of potential factors and only reported the best one, we’d be fooling ourselves. This is the multiple testing problem.

Capacity: Even if momentum works, can you trade it at scale? The biggest gains often come from the smallest, least liquid stocks.

What Quants Actually Do#

In practice, quantitative investment firms like AQR, Two Sigma, or Citadel don’t rely on a single factor. They:

Test hundreds of potential factors using tools like alphalens

Combine factors into composite signals (e.g., momentum + value + quality)

Use sophisticated risk models to control exposure to market risk, sectors, and other sources of unintended bets

Optimize portfolio construction to maximize expected return per unit of risk while minimizing turnover

Alphalens is the first step in this pipeline – it tells you whether a factor is worth investigating further. The full pipeline requires portfolio optimization (see Chapter 9), risk management (see Chapter 14), and a backtesting framework (see the BT chapter).

Tip

Try modifying the factor. Instead of 12-1 momentum, what if you used 6-month momentum? 3-month? What about a reversal factor (short recent winners, long recent losers)? Alphalens makes it easy to test these variations.